Electronic Invoicing in Belgium: An Operational Reality Check in Early 2026

- Diego Mersch

- Jan 20

- 3 min read

At the start of 2026, structured electronic invoicing is no longer an upcoming regulatory change in Belgium. It is now the standard operating framework for domestic B2B transactions between VAT-registered companies.

The legal mandate is in place. The ecosystem is active. The real question has shifted from “when will this happen?” to “how well is the market actually coping with it?”

As with most large-scale regulatory transformations, the situation on the ground is more complex than a simple compliance checklist.

Electronic Invoicing in Belgium : Registration is widespread, readiness is uneven

One of the most commonly cited indicators of progress is the number of companies registered on the Peppol network through an Access Point.

Source : BOSA & Peppolcheck

On paper, this suggests strong adoption. In practice, registration alone does not guarantee operational readiness.

Many companies are technically present on the network without having:

A fully operational outbound invoicing flow,

A reliable inbound process integrated into accounting,

Or validated end-to-end scenarios tested with real trading partners.

In some cases, registration happened indirectly via software vendors or accountants, without the company itself actively configuring or using the flow. This creates a gap between formal compliance and day-to-day usability.

Usage is increasing, but maturity varies widely

Structured invoice volumes continue to rise, which clearly shows that adoption is progressing. However, maturity levels differ significantly across the market.

Larger organisations and digitally mature companies have generally moved beyond the basics. Their invoicing flows are integrated, tested, and often embedded into internal processes.

Many SMEs, on the other hand, are still in a transitional phase. Some receive structured invoices but do not yet emit them. Others rely on semi-manual handling or temporary workarounds that technically function but do not scale well.

This imbalance is not unusual in the first phase of a mandate. It does, however, explain why operational friction remains a reality for many businesses in early 2026.

The main challenges are operational, not legal

At this stage, most companies understand the obligation. The real challenges lie in execution.

Common issues include:

Invoice rejections due to validation errors,

Confusion between structured electronic invoices and PDFs sent electronically,

Internal processes that are not aligned with structured data flows,

Accounting teams forced to intervene manually when automation fails.

The impact is concrete. Delays in processing lead to delayed payments, reconciliation issues, and unnecessary operational costs. Compliance alone does not guarantee business continuity.

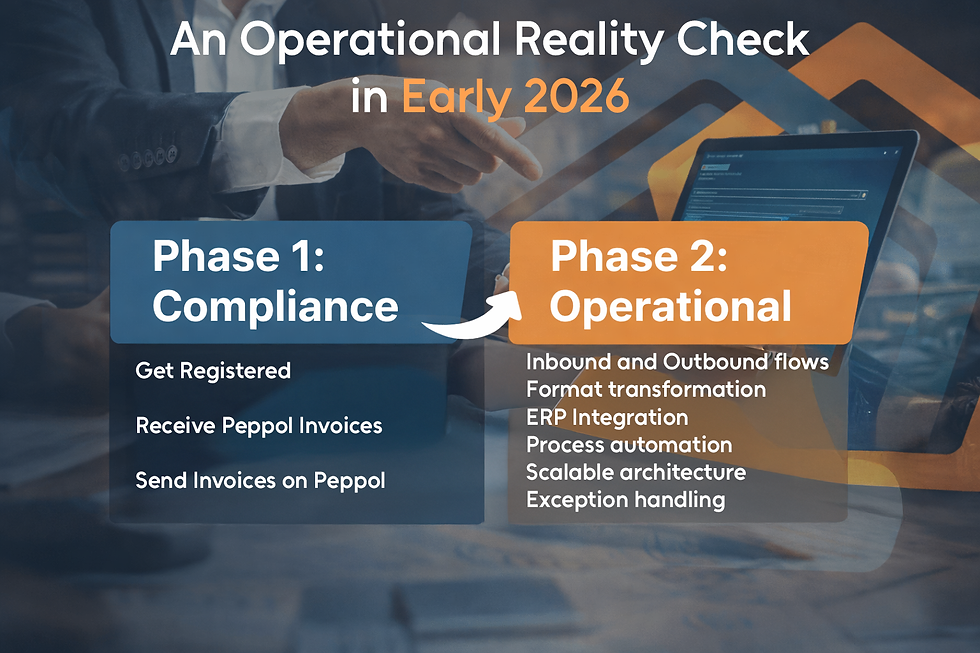

What “being ready” actually means in 2026

Preparedness is no longer about enabling a feature or signing up to a network. It is about stability and reliability.

A company can reasonably consider itself ready when:

Inbound and outbound structured invoicing flows are both active and tested,

Invoices move seamlessly from issuance to accounting without manual intervention,

Exceptions are identified, monitored, and handled efficiently,

The setup can evolve with changing volumes, partners, systems and regulatory requirements.

This is where the difference between short-term compliance and a sustainable invoicing architecture becomes very clear.

How PeppolEDGE addresses the real challenges

PeppolEDGE is designed around one core principle: operational continuity matters more than theoretical compliance.

Rather than focusing solely on network access, PeppolEDGE supports companies across the full invoicing lifecycle:

Integrating inbound and outbound flows seamlessly with ERP and accounting systems, so invoices move through existing processes without disruption.

Enabling flexible format transformations via the Bridge Module, allowing companies to convert their native formats into UBL, and to transform incoming UBL invoices back into formats that fit their internal systems or accounting tools.

Reducing manual handling and error-prone workarounds, even in hybrid or transitional setups.

Providing visibility and control over exceptions, so issues are identified early and resolved without blocking operations.

The approach is pragmatic and progressive. Companies can start with a limited scope, for example inbound readiness, then expand to outbound flows and deeper automation once the foundation is stable.

Crucially, PeppolEDGE is built to scale. As volumes grow, partners change, or future reporting requirements emerge, the platform can evolve without forcing companies to redesign their entire invoicing setup.

From mandate to infrastructure

For many organisations, 2026 will be a year of consolidation rather than radical change. The focus will be on refining processes, improving automation, and aligning internal teams around structured data flows.

Electronic invoicing in Belgium has moved beyond the project phase. It is now infrastructure, just like payment systems or accounting platforms. When it works well, it is invisible. When it does not, it becomes a bottleneck.

Conclusion

At the beginning of 2026, structured electronic invoicing is firmly embedded in the Belgian B2B landscape. Adoption is progressing, but readiness remains uneven.

The companies that will navigate this transition most smoothly are not necessarily those that moved first, but those that invested in robust, flexible, and well-integrated solutions.

Compliance may be mandatory. Operational resilience is a choice. And that is where platforms like PeppolEDGE make a tangible difference.